Secteur du numérique en France : une croissance continue depuis 15 ans qui se ralentit

Innovation, résilience et croissance durable : les maîtres-mots du secteur numérique pour 2024

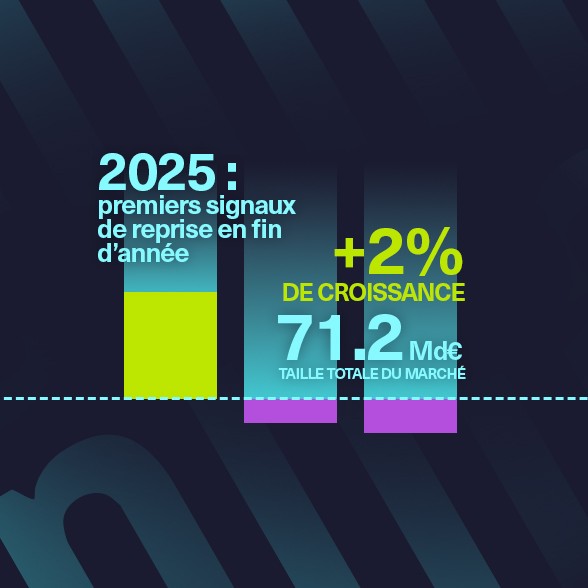

Après une croissance de +6,5% en 2023, le marché du numérique devrait croître de +5% en 2024, confirmant son rôle moteur dans l’économie française malgré un ralentissement des commandes et un contexte de marché attentiste.

Tous les métiers seront confrontés à un ralentissement de la croissance de leur chiffre d’affaires:

- Croissance estimée pour lesÉditeurs et plateformes clouden 2024: +9,6%

- Croissance estimée pour lesEntreprises de Services du Numérique(ESN)en 2024: +2,1%.

- Croissance estimée pour les activitésde Conseil en technologies(ICT)en 2024 :+3,4%

En 2024, la taille du marché du numérique est ainsi évaluée à 70,4 milliards d’euros: 38,7% du marché pour les éditeurs de logiciels et les plateformes cloud avec 27,2 milliards d’euros de chiffre d’affaires, 49,8% du marché pour les ESN avec 35 milliards d’euros et enfin 11,5% pour les activités de Conseil en Technologie avec 8,1 milliards d’euros.

Les 5 principaux leviers de croissance pour continuer de booster le numérique français

Au-delà du cloud, qui reste le levier le plus porteur pour le marché du numérique en France, des nouveaux marchés émergent, de petites tailles mais avec une croissance très forte comme le numérique responsable, et l’IA.

- Le Cloud(plateformes et services) : un marché de 39,4 milliards d’euros avec +14,2% de croissance prévue en 2024

- Le Big Data: un marché de 5,4 milliards d’euros avec +16,8% de croissance prévue en 2024. La collecte et l’usage de la donnée deviennent essentiels pour faire évoluer les business-models, développer des nouveaux services, optimiser les opérations.

- La Sécurité: un marché de 7 milliards d’euros avec +10,6% de croissance prévue en 2024. La croissance des investissements et de l’externalisation sont essentiels pour parer à la recrudescence des risques, des réglementations et des attaques.

- L’Intelligence artificielle: un marché de 2,8 milliards d’euros avec +35,7% de croissance prévue en 2024. Le sujet n’est pas nouveau mais les nouvelles technologies permettent de le démocratiser et de l’accélérer.

- Le Numérique responsable: un marché de 1,3 milliards d’euros avec +38% de croissance prévue en 2024. Un levier devenu essentiel pour la croissance des entreprises et organisations du secteur.

Fer de lance du mandat de Véronique Torner, lenumérique responsable n’est plus une option mais bien une nécessité pour les entreprises et leurs clients. Selon l’enquête réalisée par PAC pour Numeum, en 2024, 78% des entreprises du numérique prévoient d’intensifier leurs actions liées au numérique responsable, se concentrant principalement sur les aspects environnementaux. D’autre part, les entreprises sont de plus en plus sollicitées pour démontrer leurs actions en matière de responsabilité sociétale des entreprises (RSE) lors des appels d’offres. En effet, 80% des entreprises du numérique de toutes tailles répondent à des appels d’offres ayant des critères RSE. C’est près d’une entreprise sur 2 du numérique (46%) qui gagnent des projets qui portent sur un sujet de RSE.

Les talents restent la clé de la compétitivité

Face au ralentissement du déploiement des carnets de commandes, les entreprises du numérique ont été plus prudentes sur les créations d’emplois en 2023. En effet, 7000 emplois ont été créés l’an dernier contre 47 000 emplois en 2022, qui marquait un record. Il est toutefois important de préciser que les emplois créés dans le numérique le sont généralement sur du long terme: 90% de CDI et 80% de cadres.

Malgré ce ralentissement, le secteur numérique reste en tension et les besoins en compétences sont toujours importants.Les compétences les plus recherchées incluent la sécurité, le cloud et les données pour les ESN et ICT, et des équipes R&D pour les éditeurs de logiciels. De plus, les profils confirmés voire séniors sont les plus demandéspar les entreprises.

Le turnover reste structurant, en raison d’un marché ultra-concurrentiel: 45% des collaborateurs ayant quitté leur entreprise au cours des 6 premiers mois de cette année sont allés chez des clients et 43% chez des concurrents.

L’intelligence artificielle : un nouveau moteur de croissance pour les entreprises

A l’heure où l’essor de l’IA générative suscite un fort enthousiasme, l’enquête révèle un fort engouement des entreprises du numérique pour cette nouvelle ère, qu’elles considèrent comme unesource d’opportunités d’amélioration (70%) et de business (50%). Seuls 9% des entreprises du secteur considèrent que c’est une forte menace pour l’emploi. Dans le même temps,85% des entreprises du numérique ont déjà intégré dans leurs processus interne l’IA Générative en 2023 ou vont le faire en 2024 et après.

L’adoption de l’IA dans les entreprises du numérique varie selon les métiers et les processus. Si certains domaines comme le développement logiciel, le marketing et le test logiciel sont plus enclins à utiliser l’IA, d’autres fonctions comme les RH, le juridique et la finance explorent son potentiel de manière plus modérée. Les entreprises qui sauront identifier les cas d’utilisation pertinents de l’IA et l’intégrer efficacement à leurs processus seront les mieux placées pour tirer parti de cette technologie révolutionnaire.

A noter: l’enquête a eu lieu aux mois d’avril et mai 2024 et les prévisions économétriques de marché en mai 2024. Ces analyses sont donc issues du contexte économique précédent la décision de dissolution de l’Assemblée nationale. Par conséquent, Numeum et PAC restent attentifs au contexte qui pourra impacter l’activité des entreprises et potentiellement la commande publique. Lors de sa conférence semestrielle en décembre prochain, Numeum et PAC dresseront le bilan et les perspectives du marché de l’année.

Véronique Torner

Présidente de Numeum

Malgré un ralentissement, la croissance du numérique demeure remarquable. Les investissements de nos entreprises dans le domaine de la Responsabilité Sociale des Entreprises (RSE) sont judicieusement orientés, et le renforcement du développement de nos talents dans les technologies à forte valeur ajoutée et innovantes est une priorité. L’intelligence artificielle et le numérique responsable recèlent un immense potentiel pour faire de la France une grande nation du numérique. Numeum et ses adhérents demeurent vigilants face au contexte post-dissolution, qui pourrait avoir des répercussions sur l’activité de nos entreprises, notamment en ce qui concerne les marchés publics

rn